Pilots complete extensive training preparing to safely navigate challenging scenarios. This occurs BEFORE being cleared for takeoff or reviewing the first flight plan. This training enables you to remain calm and act quickly when faced with challenges.

I believe the same approach is beneficial when navigating financial markets. Helping investors prepare to avoid drawdowns and compound their returns are the primary objectives at the Knapp Advisory Group.

Before we begin, it is worth noting that warnings have varying degrees of potential outcomes. For example, ignoring a warning label that reads “cold water wash only” may result in ill-fitted clothing. Alternatively, discounting a warning label on a toaster that reads “disconnect toaster oven before cleaning” could deliver an electric shock.

Flying and investing in financial markets involve varying degrees of risk. Many investors’ financial flight plans are rarely cleared as filed. It is crucial to assess the risk of the current environment, monitor existing warning signs and adjust accordingly before deciding you are cleared for takeoff.

Carelessly, the mainstream financial media has so-called experts providing predictions. For these “experts,” these predictions have no consequences. If they’re wrong, they will make another prediction to cover the last. Expert predictions can sound like logical assumptions at first. Then, they don’t, and you reflect asking yourself, “What was I thinking?”

For the investor allocating their hard-earned assets, following predictions can have a destructive impact on both your short- and long-term financial goals. The fact remains, bull markets do end eventually! Market reversions tend to be brutal events that inflict chaos on your financial assets.

Seth Klarman from Baupost Capital said, “Can we say when it will end? No. Can we say that it will end? Yes. And when it ends and the trend reverses, here is what we can say for sure. Few will be ready. Few will be prepared.”

Remember: NO ONE RINGS A BELL AT THE TOP OF THE MARKET!

Your Part:

It is up to you, in conjunction with your investment advisor(s), to determine the acceptable risks and those related potential outcomes you are willing to encounter.

Below are data points to help you begin your financial journey.

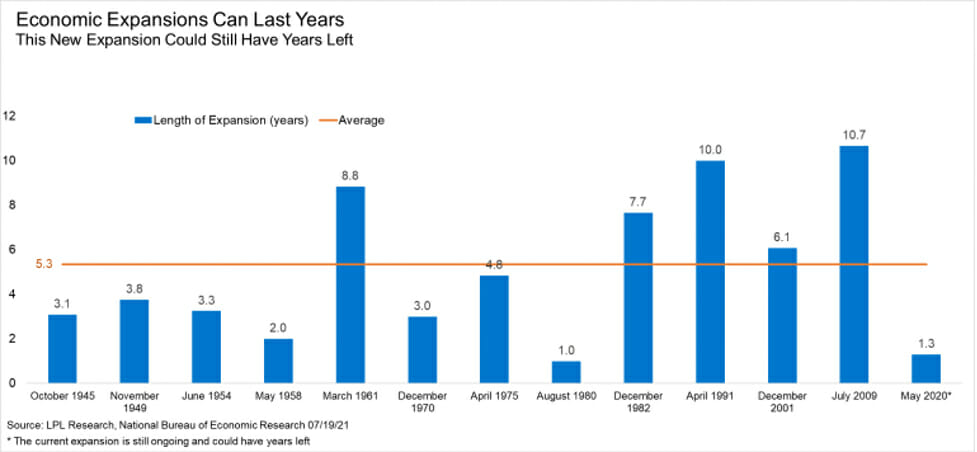

The Recession is Over (?):

On Monday July 19, 2021, the National Bureau of Economic Research (NBER) announced that the COVID recession is over, ending in April 2020. We are now in the 15th month of the new expansion. This delay is perfectly normal. NBER doesn’t change a recession call once it’s made, so they need to have a high degree of confidence in the supporting data. Waiting until 15 months after the recession to call it over is the average since they started making recession calls in real time in the 1970s.

As shown in the chart, the recession lasted only two months, the shortest on record, but also one of the steepest, the economy contracting more in just two months than any other recession back to 1948.

Though, let’s not also forget the approximately $5 trillion in direct COVID-related stimulus payments to households and businesses in 2020 and 2021. In my opinion, it is likely that there will be no further stimulus payments coming.

So, what happens now?

Based on history, it is probable that we are in for several more years of economic expansion. Expansions are on no particular timetable, but the average length of an expansion does tell us something about how long it usually takes for the kind of economic excesses to build that usually cause recessions. While post-World War II expansions have lasted as little as 12 months, the average is more than five years and the last four expansions have averaged over eight years.

Main Street Sentiment:

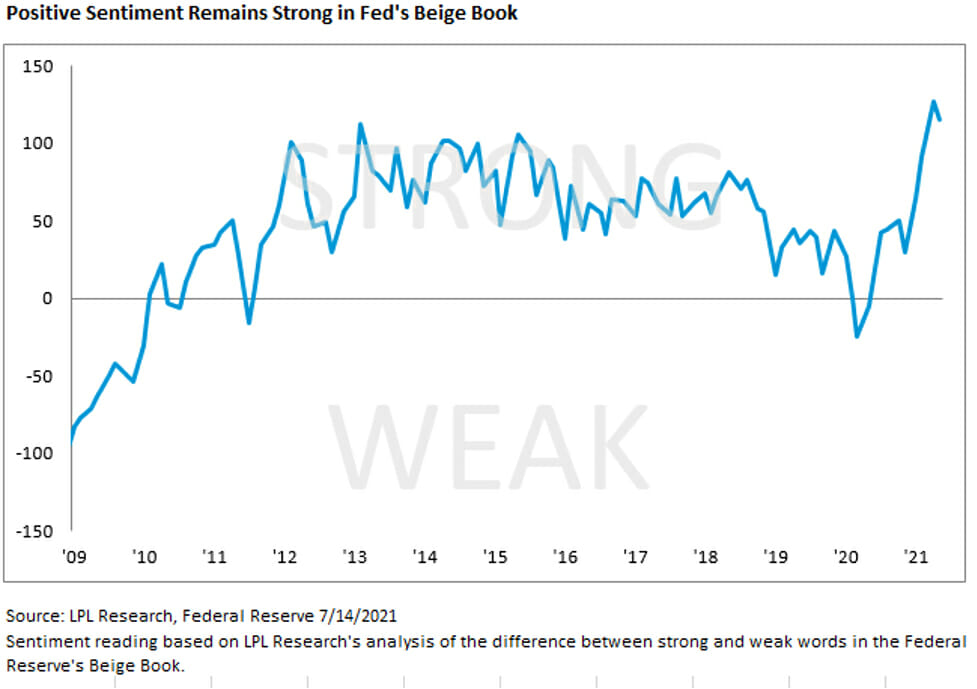

As seen in the chart, Main-Street sentiment is at its second-highest level in over a decade (according to LPL Research’s proprietary Beige Book Barometer [BBB]), topped only by the June 2021 BBB reading. The result is based on our analysis of the Federal Reserve’s (Fed) Beige Book, a publication released two weeks before each Fed policy meeting that captures qualitative observations made by community bankers and business owners – what we like to think of as “Main Street” rather than “Wall Street.” The BBB gauges sentiment by looking at how frequently key words and phrases appear in the text.

In the most recent Beige Book, “strong” words had declined slightly while “weak” words fell to their lowest level since the BBB’s inception in 2005. However, expressions of uncertainty had increased and the report did note broad-based pricing pressures. Our sub-index of inflation-related words in the Beige Book remained at its highest level since we created the inflation sub-index in 2015.

Inflation:

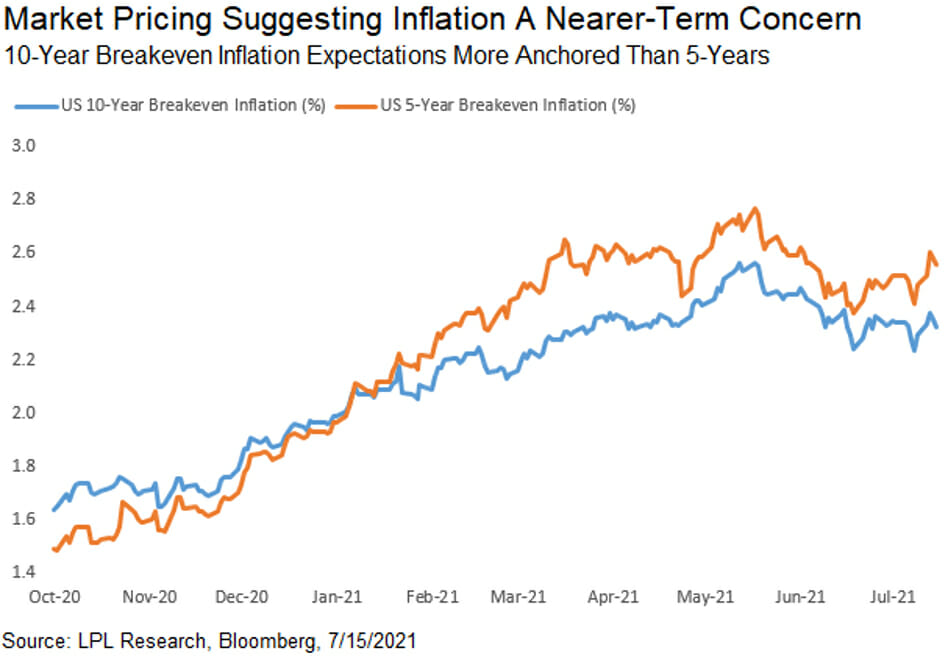

Breakeven inflation rates, market-based measures of inflation expectations over given timeframes, rose steadily until roughly the release of the April CPI report when we started hearing about peak inflation concerns. Though that report beat consensus estimates, the subsequent drop in both five- and ten-year breakevens suggests the market accepted the Fed’s characterization of inflation as transitory.

And while the levels of these series can be volatile, we believe the divergence that began around the New Year is telling. Five-year breakevens began outpacing ten-year breakevens, suggesting that inflation may run hotter in the near-to-intermediate term, but that the market still has faith in the Fed to keep long-term inflation under control. Five-years making a new local high in the last week without ten-years following suit suggests that while the market is slightly concerned that transitory may prove to be longer than originally thought, it does not believe it will cause concerns on a longer horizon.

According to BTN Research, in the last 70 years (1951-2020), inflation as measured by the “Consumer Price Index” (CPI), has been at least 5+% in 12 different years, most recently in 1990. The S&P 500 has been equally split over the 12 high-inflation years, advancing in six years and falling in six years (on a total return basis). The average return for the S&P 500 over all 12 years is a gain of just +3.2% (total return).

Fewer Stocks Making New Highs:

The S&P 500 Index has hit new record highs, but under the surface, fewer stocks have been participating. Just 15% of the stocks in the index hit a new one-month high along with the benchmark on June 24, and for the first time since December 1999, a record-closing high occurred with less than half of the stocks in the index above their 50-day moving averages. If the last few years have taught us anything, it should be that the largest technology stocks are capable of powering the S&P 500 to new highs. However, a far healthier and more sustainable trend typically sees stronger participation, like earlier in the year when new highs in the S&P 500 were commonly accompanied by 30-40% of the index hitting new highs as well.

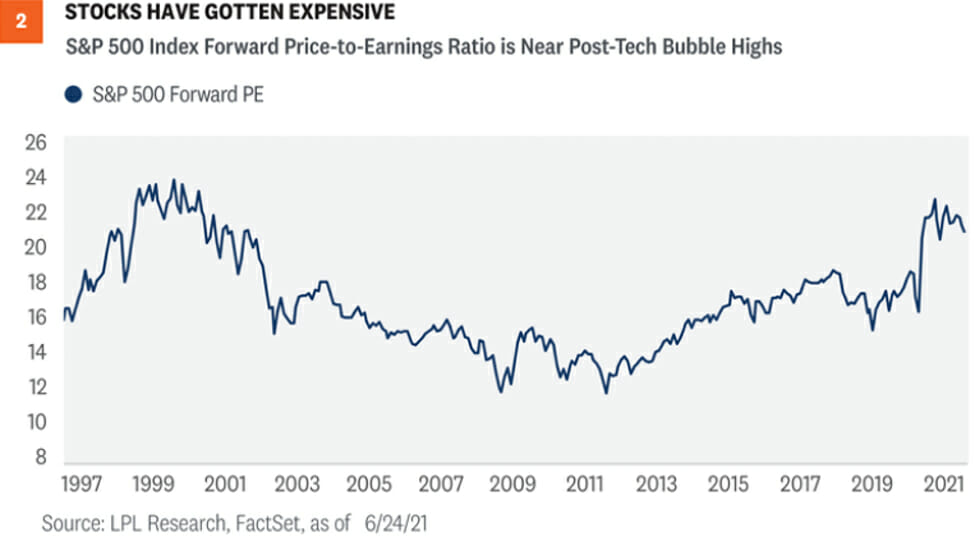

Elevated Stock Valuations:

Thanks to the strong start to this bull market, stock valuations have become a widespread concern. Although valuations have not historically been good short-term timing tools for investors, when a downside catalyst eventually emerges, a more richly valued stock market tends to sell off more. After a big rally, more optimism is priced in, and that higher bar then opens the door to disappointment.

The Knapp Advisory Group’s primary objectives are helping investors work towards avoiding drawdowns and compounding returns. For more education, contact at JAMES.KNAPP@KNAPPADVISORY.COM.

James C. Knapp, AIF®, BFA™, CPFA®

Securities and advisory services offered through LPL Financial, a Registered Investment Advisor, Member FINRA/SIPC

The material and opinions expressed here are for general information only and are not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

Generally, references to markets, asset classes, and sectors regard the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial does not provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

Bloomberg Barclays Global Aggregate Negative Yielding Debt represents the negative-yielding segment of the global investment grade debt from 24 local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging market issuers.

Portions of the materials have been prepared by LPL Financial

{kind=link}