I just returned from annual training for my airline. It’s nice to have another year before I have to study again, right? ( I’m kidding, of course!) Every year in training we discuss human factors, crew resource management, and the Risk and Resource Management (RRM) model that’s been in the airline world for some time now. I was interested to learn, that in addition to our RRM model, next year’s training syllabus will include even more material on mental models; the way we think in the cockpit, how we work together, etc. Many of you know this as human factors and crew resource management (CRM).

Additionally, it appears the airlines are learning that incidents and accidents don’t happen due lack of technical or flying expertise but are owed to poor decision making as a result of one’s current state of mind. I know all this may sound crazy to some pilots but the evidence is compelling as well as interesting.

What in the world does this have to do with your personal finances and investing? Everything! We’ve all learned in our flight training that small changes in crew behavior make flying the airplane safer. The same is true when it comes to retirement planning. Making small changes in the way you think, behave (human factors) and make decisions, will improve your chances of successful retirement planning and investing.

Studies clearly demonstrate that we are programmed with behavioral biases that help us survive and thrive in life. Some of these behaviors serve us very well in most aspects of our lives. Unfortunately, these same behavioral biases often sabotage our attempts at saving for the future and achieving the highest level of investment return available to us in the markets.

A recent study by the National Bureau of Economic Research (NBER) demonstrated that our behavioral biases could be costing us a lot of money when it comes to achieving our highest potential in our 401(k) and retirement plans. For example, according to the NBER study, the “present bias,” along with other biases, are holding back millions of Americans from saving enough money for retirement.

From the Bloomberg article on the same topic; “…How much money? Try $1.7 trillion on for size. That's 12 percent of the $14 trillion in U.S. individual retirement and 401(k) accounts.”

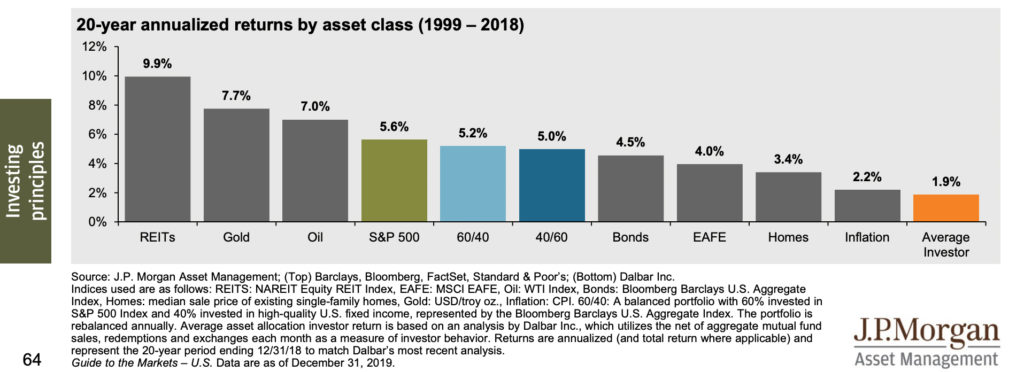

Dalbar Inc. annually releases a study that shows how the average equity investor’s investment performance stacks up against different equity indices. According to Dalbar, for the 20-year period ending 2018, the average equity investor earned a compound annual return of 1.9% versus the S&P 500 Index that returned an annual compound rate of return of 5.6%. (Interesting side note: This 5.6% rolling 20-year U.S. Stock return is one of the lowest since the 1950s!)

Clearly, we’re all above average investors, right? Other studies showed when a group of participants was asked if they were above average drivers over 80% of the group claimed to be above average drivers. Yes, you guessed it, this is another one of our well-researched behavioral biases called the “overconfidence bias.”

One final example that I can’t help but share is the “optimism bias.” This bias is absolutely necessary in our everyday lives. After all, who wants to be around a pessimist all the time? Furthermore, those who lack the optimism bias are more prone to be depressed.

On the other hand, when this bias is applied to our financial life it can lead to negative results. In a Ted Talk I recently viewed given by Tali Sharot, she stated that 80% of us have the optimism bias. The optimism bias sometimes causes us to think the future will turn out to be better than it actually does.

How many of you, as I was doing in the late 1990s right out of college, were projecting investment returns to be a “conservative” 15% annually? That’s a pretty optimistic (unrealistic) view of the future! As a young second lieutenant, I thought I would be ready to retire from the Air Force after ten years of service. Not so! Of course, there were other factors (behavioral biases) that caused me to be overly optimistic, even unrealistic, but this extreme example illustrates the simple truth.

Large organizations understand that our optimism bias can lead to faulty planning and therefore they factor that into the planning process. We should do the same.

So what should we do about the harmful effects of these biases?

1. Know thyself!

- We must be aware that some of the attitudes and beliefs that serve us so well in most aspects of our lives tend to work against us when it comes to investing and saving for the future.

- Investing and saving for the future requires a different way of thinking, often counter-intuitive, in order to be successful.

- We must strike a balance between the good that comes from our optimism, overconfidence, etc., and the harm it can cause when it comes to investing and retirement planning.

2. You must have a plan for your future.

- Simply put, those that have a plan, set goals and make decisions based on reaching their financial goals will do better than those who do not.

- Do not base your plan on overly-optimistic assumptions. We want to know: Does the plan hold up under difficult circumstances?

- Act like a contingency planner. Always ask yourself; what could go wrong in the future? What has actually happened in the past and could it happen again? How will that affect my desired result or goal?

3. Control the controllable.

- Use your valuable time, energy and other resources to control or worry about things that you have some control over. In other words, don’t waste your time and mental energy trying to control the short-term performance of the stock market. In the short term, the stock market is uncontrollable as well as unpredictable.

- On the other hand, there are many things that are within our control. Knowing and paying attention to the things that are within our circle of influence can have a dramatic impact on our quality of life now and in retirement. For example: How much we save, spending habits, proactive tax planning, low-cost investing, etc.

4. Don’t operate in a vacuum.

- Seek out trusted counsel, friends, family, and advisors.

- Successful business CEOs, athletes, and musicians have coaches and mentors and so should you.

- Anyone who’s trying to do something difficult and important should not operate in a vacuum.

Luckily for us, we don’t have to be Chuck Yeager to fly our passengers safely from Chicago to Los Angeles. (Although, clearly, we’re all above average airline pilots!) Likewise, we don’t have to be Warren Buffett to have a great airline retirement and achieve solid investment returns. As demonstrated in this article, one of the most important areas to focus on to help you reach your financial goals is not a secret investing solution or silver bullet. We must focus on our own behaviors!

{kind=link}